The Current State Of Networks

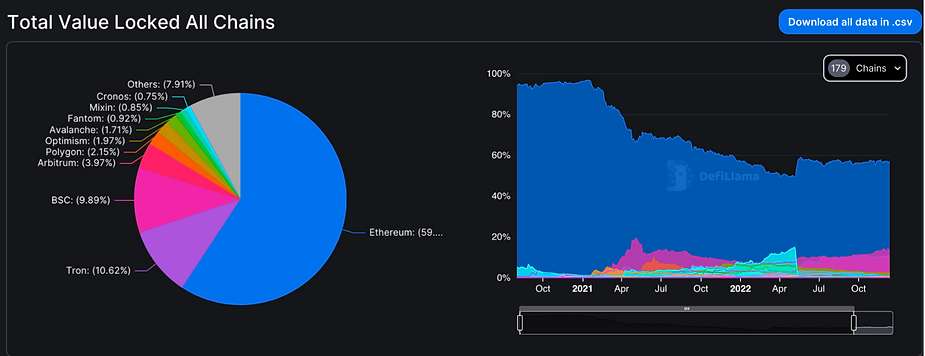

Total value locked (TVL) in the cryptocurrency space does not exist solely on the Ethereum network. As seen in Figure 1, while most TVL (59%) lies on Ethereum, the remaining 41% is spread across over 179 chains, with an increasing number in development daily. Our previous article highlighting our latest investment, Orb Labs, we wrote about a multi-chain future. However, this fragmented liquidity poses an issue for developing novel applications.

Figure 1: TVL Across Chains, DefiLlama

Creating a new layer 1, or any application that cannot be deployed on top of the Ethereum virtual machine (EVM), requires actively validated services (AVS) secured mainly by their respective native tokens. Take Solana, for example – as seen in Figure 2, with over 500,000 unique active stakers and over 8 billion in $SOL staked, deploying a new, non-EVM layer 1 is extremely capital intensive. It requires willing market participants who may incur losses of capital or time, all to validate the network.

Figure 2: Data On Solana Validators, SolanaCompass

While networks like Solana and Aptos have significant venture capital backing, automatically giving them willing participants to validate their networks, many newer layer 1s and dApps do not have this luxury.

On top of facing bootstrapping and capital cost issues, AVS are incredibly susceptible to attacks due to them requiring completely new validators. – As such, for Proof-of-Stake networks that issue their native token, they have to accrue a large amount of value to have adequate security.

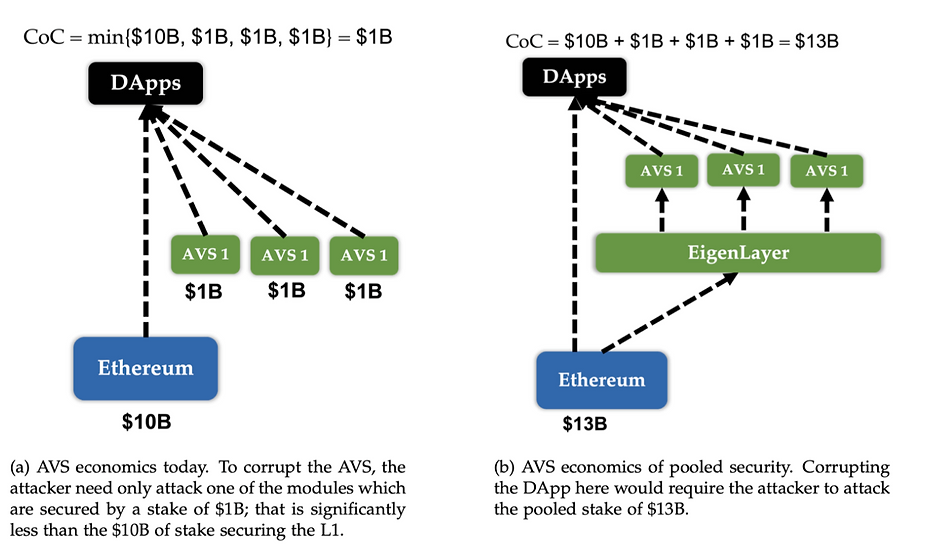

In a sense, they are starting anew, hence, for these smaller validator networks, the cost of corruption is much cheaper than if someone were to try to attack the Ethereum network. We can look to Figure 3 for an illustration of this, courtesy of the Eigenlayer Whitepaper.

Figure 3: Cost of Corruption Of Individual Validators Versus Pooled Security, Eigenlayer

Eigenlayer

Introduction of Eigenlayer

EigenLayer – an Ethereum restaking protocol, recently announced a $50 million Series A fundraising led by Blockchain Capital. For those unfamiliar, Eigenlayer hopes to aggregate the fragmented trust and liquidity across all disparate networks. In addition, by introducing a set of smart contracts on Ethereum, Eigenlayer allows existing consensus layer ETH stakers to opt-in to validate new software modules built on top of the Ethereum ecosystem.

Figure 4: EigenLayer Restaking

In simple terms, this means that existing ETH stakers can choose to opt-in by granting the smart contracts the ability to impose additional slashing conditions on their staked ETH. In return, the stakers can gain additional revenue from providing security and validation services to the chosen modules. The type of modules can range from side chains to data availability layers, virtual machines, and more.

Then, a mutually beneficial relationship between developers and validators is formed. By utilizing the comparatively secure validators on Ethereum, new AVS do not have to branch out and raise capital for their own validator set. In return, existing market participants will not have to split their capital and resources to other networks but can aggregate their liquidity on Ethereum.

This adds the hidden effect of creating a positive flywheel where incentives align. As more teams use ETH validators, ETH stakers get a higher return. – As more people are incentivized to stake ETH, this further increases the security of Ethereum and other EigenLayer projects.

In the words of the EigenLayer team: “EigenLayer serves as an open marketplace where AVSs can rent pooled security provided by Ethereum validators.”

Risks

The EigenLayer team has outlined two categories of risk:

1. Collusion of operators to attack a set of AVS

Realistically speaking, not all ETH stakers will opt-in to EigenLayer, and some may even choose different AVS to stake into.

For example, consider an AVS secured by $8M of re-staked ETH with a TVL of $2M. A successful attack would require at least $4M of the attacker’s stake to be slashed, making the attack economically unviable. However, if this same ETH is re-staked in 10 other AVS, each of which has $2M locked, the total profit from corrupting this group of re-stakers is $20M, with only $8M at stake.

To mitigate this risk, the EigenLayer team has proposed two solutions. The first is to add specifications to service contracts by restricting total value flow or total value transacted within a certain period.

The second solution relies on creating an open-source dashboard to monitor the set of operators participating in validation tasks. By putting certain conditions in place, such as only allowing operators who are participating in a low number of AVS, thus prevents validators from being too heavily entrenched in multiple AVS.

2. Unintended slashing due to smart contract risk

The second risk mainly applies to new AVS without battle-tested code. When deploying new applications, there is a chance that an AVS with an unintentional slashing vulnerability (ex., a programming bug) gets triggered and causes the loss of funds.

Like any application on the blockchain, smart contract risk is highly prevalent. As such, the EigenLayer team proposes two lines of defense: audits and the ability to veto slashing events. While this might sound contrary to the idea of decentralization, the EigenLayer team sees this as training wheels that will eventually be removed. The veto committee will comprise reputed individuals in the Ethereum and EigenLayer committee and will not hold the power of maliciously triggering slashing. They will only be able to veto a slashing if it accidentally occurs. Once the AVS is considered mature and battle-tested, the AVS can stop using the veto committee as a failsafe.

Concluding Thoughts

In our recent article on Liquid Staking, we reinstated our belief in the growth of the Liquid Staking ecosystem as a whole – EigenLayer takes this further. It creates more economical applications for staked ETH, greatly expanding the staked ETH market.

While the technology is still in its testing stages, it is an exciting innovation that aligns both users and developers of Ethereum. Eigenlayer represents a new opportunity for market participants to stake their ETH for the long term, generating the positive flywheel effect as mentioned above.

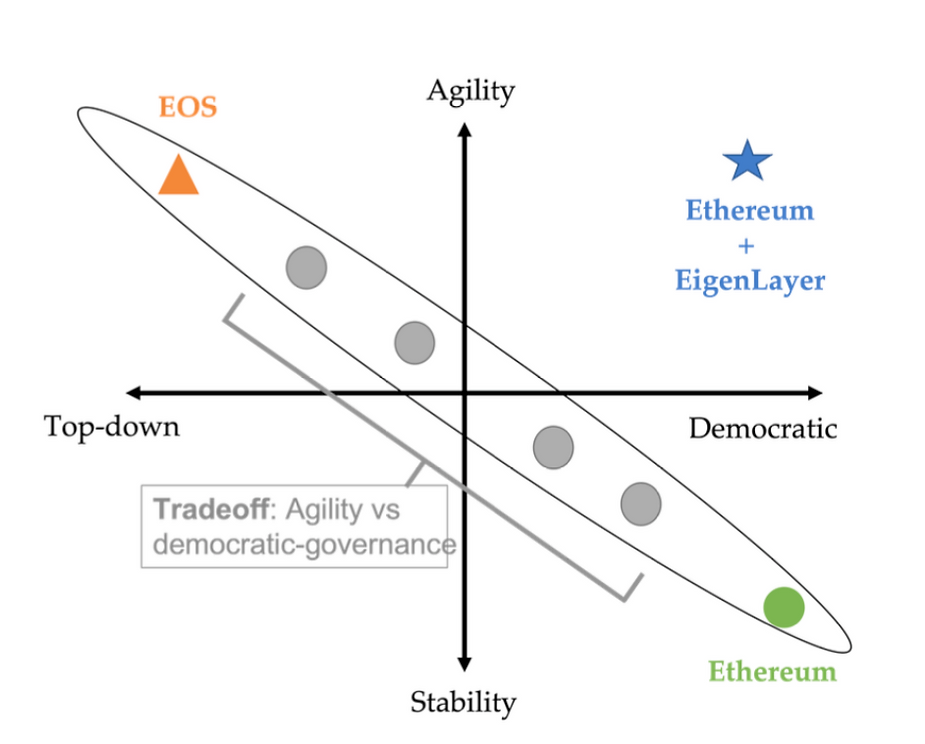

Figure 5: Tradeoffs between democracy and speed, EigenLayer

While the Ethereum network currently enjoys democratic and stable development, innovation on top of the chain is slow. With EigenLayer eliminating the need for new applications to ensure security by starting from the ground, we believe this product can potentially pave the way to more democratic, agile, and rapid innovation without sacrificing stability.

Disclaimer: This material has been shared solely for information purposes, and must not be relied upon for the purpose of entering into any transaction nor investment. Newman Capital is not an investment adviser, and is not purporting to provide you with investment, legal or tax advice. You are always advised to DO YOUR OWN RESEARCH before making any investment decision. Newman Capital is an investor in Openfort.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}