Introduction

Capital inefficiency and price discovery are the two main hurdles that create illiquidity for NFT assets. Users can only recently deposit their previously illiquid assets into the DeFi ecosystem to generate income and provide liquidity. Today, we will look into the state of NFT lending, which is a crucial part of the financialization of NFT, and the solution to the illiquidity problems of NFTs. We will start by illustrating two major types of lending models and then elaborate on our prediction within this space of the crossover between NFT and DeFi.

Traditionally, an illiquid asset refers to an asset that cannot be easily sold or traded without a significant discount. Real estate, collectible automobiles, antiques, and art collectibles are some common examples of illiquid assets. Trading of these assets usually takes months or potentially longer to find a buyer. For this reason, since the 1970s, intermediaries such as banks and auction houses have provided liquidity to an exclusive audience so people can extract value from their illiquid assets by using them as loan collateral.

Today, non-fungible tokens (NFTs), an emerging asset in the crypto space, are facing similar issues. NFTs consist of digital data stored on the blockchain, representing property rights, uniqueness, and a level of illiquidity comparable to fine art and collectibles. While we can sell fungible tokens like BTC and ETH almost instantly in the market, it takes much longer to sell NFTs in any secondary market. As a result, NFT lending protocols have emerged as a liquidity solution for this digital asset.

Currently in an early development stage, NFT lending has plenty of room for growth. As of 14 July 2022, the total NFT market is worth $22.98 billion, reaching a provisional peak of $35 billion in January 2022. Blue-chip NFT collections, which most lending protocols now support, represent 30% of the market. With the expectation that more collections will be approved in the near future and more DAOs exploring the concept, the lending sector is anticipated to grow significantly larger and play an increasingly important role in the broader NFT landscape.

What is NFT Lending?

NFT lending protocols have a similar lending mechanism to that of DeFi lending protocols, which enable users to lend and borrow crypto assets in a trustless manner without relying on intermediaries like banks. In most cases, these DeFi platforms require over-collateralization of loans. Users typically deposit crypto like ETH or stablecoins like DAI or USDT as collateral. In the case of NFT lending, NFT lending protocols allow users to collateralize NFTs to unlock liquidity from them.

Peer-to-Peer (P2P) Lending Model

Similar to DeFi lending, there are also a few lending models that work well with NFTs, one being peer-to-peer (P2P) NFT lending.

P2P lending recreates the classic model of centralized lending by matching borrowers and lenders. When an agreement is reached between borrowers and lenders, the loan is executed. This model gives freedom to both parties because everything, including the annual percentage rate (APR), loan terms, and loan-to-value (LTV) is customizable. Let’s look at several NFT lending protocols that leverage the P2P lending model.

NFTfi

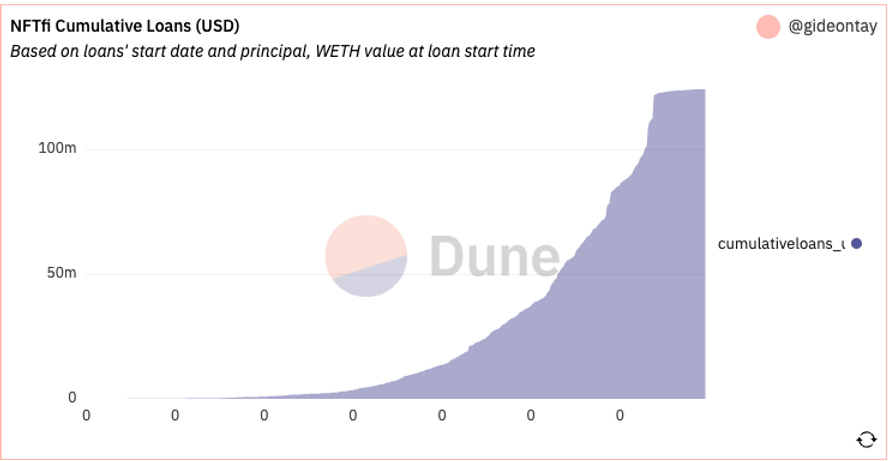

NFTfi is a P2P NFT lending platform that allows borrowers to collateralize their NFTs to borrow loans while lenders earn interest by lending out their NFTs. It is the leading NFT lending protocol by volume. As of 13 July 2022, it has facilitated over $123 million.

Figure 1: NFTfi Cumulative Loans since launched

In NFTfi’s P2P model, the borrowers list their NFT as collateral and modify the loan amount, duration, and APR. The lenders can accept the terms and loan out either wETH or DAI. They can also make a counteroffer, which will be down to the borrowers to take. Once a party accepts the offer their counterparty makes, the loan will be executed, and the NFT collateral will be sent to an escrow smart contract. The borrowers can get back the NFT collateral if the borrowers repay the loan on time. Otherwise, the NFT ownership will be transferred to the lenders.

The NFTfi team took a unique approach in terms of the liquidation mechanism. They abandoned the automatic liquidation that is typical in crypto collateral lending platforms. Instead, with NFTfi, a liquidation will not be triggered by the value of the collateral going below a certain point, but only by the borrower’s failure to repay the loan and interest at expiry.

As there is no automatic liquidation in NFTfi and the APR and LTV are set by either the borrowers or lenders, the NFT pricing is, in a sense, implicitly determined by the users. As long as both parties agree on the terms, the loan will be executed. In addition, the protocol provides data like floor price, last transaction price, and valuations by analytics platforms for users to reference on their offer page.

Arcade

Arcade is another NFT lending protocol based on the P2P lending model. It works the same as NFTfi in the lending mechanism: the borrowers create a loan request with loan terms and APR, and the lenders can accept or choose to make an offer on their request. When both parties agree on the terms, Arcade will execute the loan. In the case of default, the ownership of the collateral will transfer to the lender.

What distinguishes Arcade from NFTfi is that the former supports users to put ERC20, ERC721, and ERC1155 assets in a basket as collateral through a wrapper ERC721 contract. In contrast, the latter allows only a single token of the ERC721 standard. This asset wrapping feature means that users can take out a larger loan by collateralizing multiple assets with different token standards in a single loan.

Figure 3: Arcade User Interface

Liquidity-Pool (LP) Lending Model

Unlike the P2P model, there is no such interaction between borrowers and lenders in the liquidity-pool (LP) lending model. It allows users to deposit their NFTs and borrow directly from the pool. This model requires liquidity providers to pool their assets.

JPEG’D

JPEG’d has developed a DeFi primitive, non-fungible debt position (NFDP), intending to bridge the gap between DeFi and NFTs. The protocol lets NFT owners deposit their NFT in a smart contract to earn yield. Although there is no “liquidity pool” on JPEG’d, it is categorized as an LP lending model for better understanding because NFDP shares many similarities.

The NFDP works like the collateralized debt position (CDP) on MakerDAO. After the NFT holders deposit their NFT as collateral in the liquidity pool, they will be able to mint PUSD, a synthetic stablecoin backed by crypto assets. Holders must pay a 0.5% withdrawal fee plus any accrued interest (the APR will be dynamically adjusted) if they want to close their debt positions to reclaim their NFT from the pool.

Moreover, they allow a maximum of 32% of the collateral value to be drawn (or a 300% collateral ratio), which means that their positions will be liquidated when the LTV ratio exceeds 33%. The DAO can choose to hold the NFT or resell it on a secondary market. To secure their assets, holders have an option to purchase insurance with a 1% non-refundable fee. If their positions are liquidated, they can choose to repurchase their NFT from the DAO after repaying debt and accrued interest with a 25% liquidation penalty.

JPEG’d is working with Chainlink for the valuation of the NFTs as collateral. The Chainlink Price Feed, a custom oracle solution for pricing NFTs, will quantify the time-weighted average price (TWAP) of both sales and floor prices for the valuation. The oracle excludes wash-sales and outliers to provide a more accurate valuation, thus playing a foundational role in the functioning of liquidation and determining the maximum size of the loan position.

A specific case demonstrates the price difference between using the JPEG’d oracle vs an NFT marketplace. On 13 July 2022, the floor price of Cryptopunks was at 76.48 ETH on JPEG’d while the 7-day average price of the collection on Opensea was 93.63 ETH. Bored Ape Yacht Club (BAYC) was priced at 99.37 ETH and 125.00 ETH, respectively.

Figure 4: JPEG’d User Interface

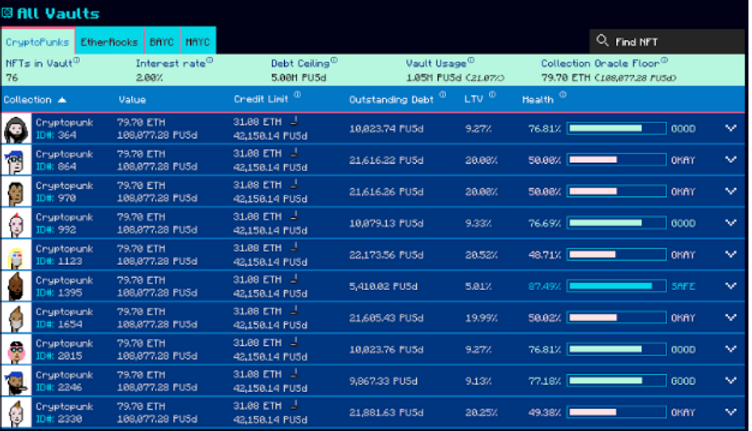

BendDAO

BendDAO is the first LP-based NFT lending protocol. Although its lending mechanism is similar to that of JPED’d, there are differences between the two protocols.

BendDAO is unique in terms of its liquidation mechanism. When liquidation occurs, the NFT will automatically go to auction. If the borrower fails to repay the loan and liquidation penalty within 48 hours, the last bidder pays back the loan and receives the NFT as collateral. For users to secure the NFT assets deposited in the pool, there is a 48-hour liquidation protection instead of insurance. When liquidation occurs, the holders can choose to repay the loan within 48 hours to reclaim their NFT.

BendDAO also introduced boundNFT, a debit note minted when the loan is lent out. It allows users to enjoy the benefits of holding their NFT even when deposited as collateral in the pool. They can still receive airdrops, claims, and mintable assets that come as a result of holding their NFTs. For instance, if you hold a BAYC and collateralize it, you can still receive airdropped Apecoin and other holder benefits. Additionally, they allow users to use the collateralized NFTs to claim third parties airdrops without repaying the loan through a flash claim, which functions similarly to a flash loan on DeFi lending protocol.

In terms of the valuation method, BendDAO works like JPEG’d. They use NFT floor prices from OpenSea and LooksRare, and calculate the TWAP to filter outliers.

Both LP lending model-based protocols JPEG’d and BendDAO have their governance tokens, JPEG and veBEND, respectively. These tokens enable holders to participate in the decision-making processes of their DAOs, such as deciding which NFT collections can be accepted as collaterals. With BendDAO, users have to stake their BEND in exchange for veBEND to earn protocol revenue and voting power. For JPEG’d, users can create or vote on governance proposals as long as they hold JPEG.

Figure 5: BendDAO User Interface

The NFT Lending Landscape

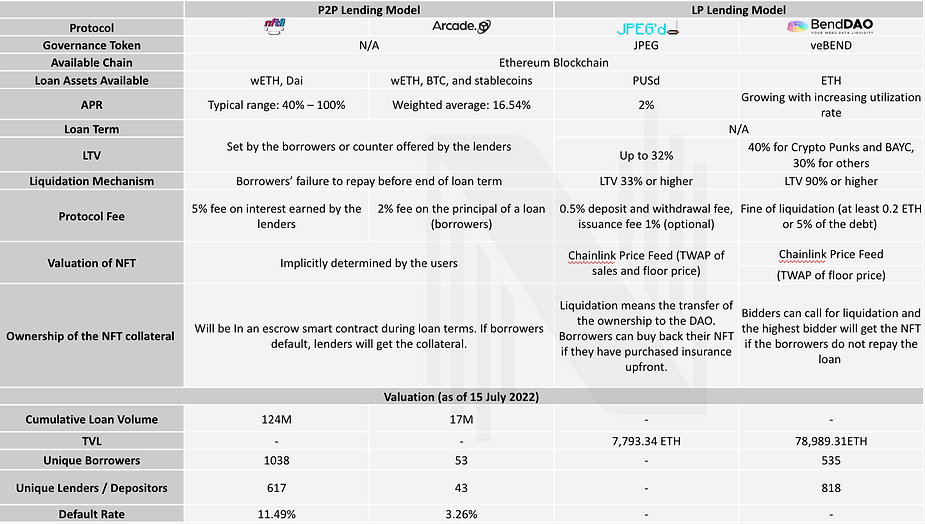

A comparison between the four NFT lending protocols mentioned above:

These protocols offer opportunities for borrowers to leverage their NFTs and for lenders to earn yield. However, these protocols may face some resistance due to the nature of their lending models.

Comparing P2P and LP Models

In terms of their valuation mechanism, the P2P model enables custom pricing for NFTs which more accurately values NFTs to their market price as there must be a price agreement between borrowers and lenders. Contrastingly, the LP model prices NFTs with the TWAP of the floor prices or historical transactions through an oracle which equally values every NFT from the same collection. For example, according to Trait Snipper at the time of writing, Bored Apes with the dagger-in-mouth trait have a floor price of 289 ETH while the full collection’s floor price sits at 93 ETH. Though a BAYC with a rare trait can be sold at a higher price than a floor Ape, the LP model would value both loans equally. This deincentivizes borrowers with rare or more desirable NFTs from using LP over P2P models.

In terms of user experience, it is noteworthy that the LP model has an edge in terms of convenience. For instance, if a holder wants to borrow a loan in a short time frame, they do not have to wait for acceptance from a counterparty. Instead, they can directly deposit their NFT as collateral in the pool in exchange for more liquid crypto assets.

Lastly, the risks for lenders are different in these two lending models. In the P2P model, borrowers can decide whether they’d like to default on purpose when the value of the collateral drops below that of the loan, while the lenders have virtually no control over their lent out assets. Risks for the LP model are similar to those of other DeFi liquidity pools: default, stablecoin, and rug pull risks.

Our NFT Lending Prediction

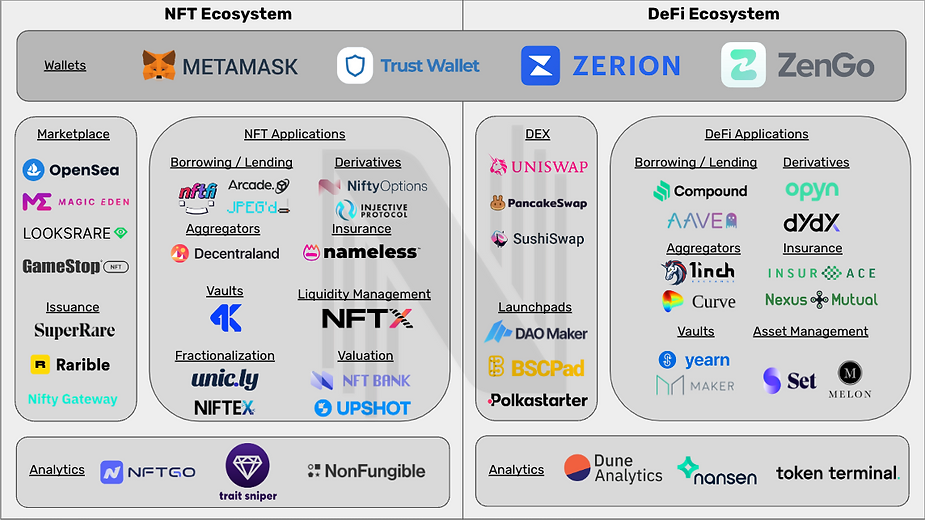

In 2020, we saw DeFi summer and its solutions to long-standing problems in the traditional financial industry. In 2021, we saw the booming of NFTs and their use cases across various applications. At earlier stages, most of these applications take after verticals in the DeFi space. Examples include lending, derivatives, and insurance.

The figure below provides a broad view of the verticals in NFT and DeFi ecosystems:

As the space and its users continue to mature, it is expected that NFTs will continue to expand their practicality across different areas and eventually develop a full suite of more accessible services. The financialization of NFTs will play an essential part but this does not merely include NFT lending – this is just the beginning of the progression. In the future, we will see new approaches to the financialization of NFTs, such as NFT perpetual contracts, yield aggregators, or many other derivatives.

Additionally, the newly introduced standard ERC4907 will primarily benefit the operation of NFT lending as a new contract extension of the ERC721 standard. This new standard facilitates the process of NFT lending by incorporating an additional “user” role and “expire” time that is revoked automatically into the smart contract. It happens in a single transaction when the NFT owners lend out their NFTs to borrowers (or “user”), and the NFT automatically returns to the owners when the loan term ends (or “expires”). This standard written on the smart contract means that NFT lending protocols can implement this new contract extension directly. It will help facilitate the operation of the NFT lending process and unlock many potential applications of this vertical in the NFT ecosystem.

Conclusion

The problems with illiquid assets have long existed in history and NFT lending protocols are just the latest solution to support financialization of this rapidly growing asset type. Although the financialization of NFTs is not as mature as DeFi, lessons learned in the DeFi space have allowed NFT builders to avoid similar development mistakes.

On top of DeFi’s foundation, we have seen innovations thanks to the nature of NFTs. For instance, Arcade enables users to collateralize a basket of tokens in different standards and BendDAO introduced boundNFT that allows borrowers to receive all the benefits for holding an NFT even during the loan term. As we advance, it is believed that there will be more DeFi-based use cases for NFTs in the near future. Furthermore, increasing DeFi-based use cases for NFTs can strengthen the role of DAOs as communities are expected to be more involved in governance issues and the decision-making processes. These emerging solutions will not only diversify NFT utility, but will also bring innovation to the NFT and wider web3 space.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}